NATIONAL SURVEY: Two-Thirds of Middle-Income Americans Feel School Failed Them on Financial Education, with Youngest Most Challenged

60% say they are not saving enough for retirement

DULUTH, Ga.--(BUSINESS WIRE)-- Primerica, Inc. (NYSE: PRI), a leading provider of financial services and products in the United States and Canada, released its Financial Security Monitor™ (FSM™) survey for the first quarter of 2024, revealing two-thirds (66%) of middle-income Americans feel their education did not adequately prepare them to manage their finances as adults, with a notable discrepancy across age groups.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20240408765232/en/

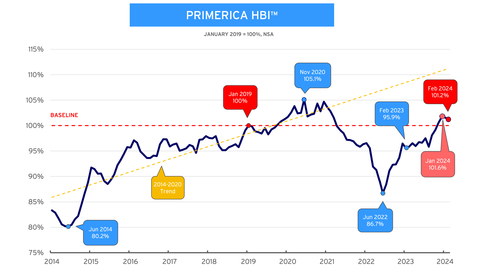

Primerica Household Budget Index™ - In February 2024, the average purchasing power for middle-income households was 101.2%, slightly down from 101.6% in January 2024. A year ago, the index stood at 95.9%. (Graphic: Business Wire)

A majority of those under age 65 said their financial education fell short, with the youngest age brackets expressing the highest level of dissatisfaction, including 73% of those ages 18-34, 69% of those 35-49, and 65% of ages 50-64. In contrast, a majority (61%) of men over 65 felt their education did a good job preparing them — the only demographic to believe so — while a majority (57%) of women in the same age group said the opposite.

Specifically, most middle-income Americans said schools did not prepare them for tasks such as doing taxes (71%), paying back student loans (67%), taking out and paying back loans (64%), or setting a household budget (59%).

“We are seeing a clear lack of confidence among middle-income Americans who believe their education failed to prepare them to manage their personal finances, with an overwhelming majority of young people feeling left behind,” said Glenn J. Williams, CEO of Primerica. “These are gaps we have to recognize and address as people plan their financial futures and navigate a fluctuating economic environment that, in recent years, has left middle-income Americans feeling incredibly uncertain about their financial situations.”

The latest FSM™ survey coincides with the release of Primerica’s Household Budget Index™ (HBI™), which indicates middle-income households experienced a slight dip in purchasing power after a stronger start to the year, as rising costs for necessities like gas slightly outpaced income gains. The HBI fell to 101.2% in February from 101.6% in January but is still up notably from 95.9% compared to one year ago.

“Gas price increases are often immediately felt by middle-income Americans, with a direct impact on their purchasing power with every fill-up. Relative to a year ago, middle-income households are doing a bit better as the prices of most necessities have increased only a small amount and gasoline has come down some while incomes have risen at a faster pace on average than overall inflation,” said Amy Crews Cutts, Ph.D., CBE®, economic consultant to Primerica. “While the slight loss of purchasing power for middle income households from January to February is equivalent to the cost of a fancy coffee drink, it is a reminder that inflation is still troublesome for households trying to keep a budget and plan for their financial future.”

Key Findings from Primerica’s U.S. Middle-Income Financial Security Monitor™

- Schools fall short on financial education, with generational divide. The majority (66%) of middle-income Americans feel the education they received during their upbringing didn't equip them to manage their finances as adults. Nearly half (49%) say that it did not prepare them well at all, with a third (33%) saying it prepared them very or somewhat well.

- Middle-income Americans are increasingly concerned about credit card debt. More than a third of middle-income Americans (38%) are more concerned about their credit card debt compared to a year ago. A majority who feel this way also report spending less overall (71%, up 9 points since December 2023), and some say they are looking at additional income sources (32%, up 6 points) or debt consolidation (16%, also up 6 points).

- Most middle-income Americans merge finances with their partner after marriage. About three-quarters (73%) of married Americans merge their finances with their partners, a fifth (20%) keep their finances separate from their partner, and less than a tenth (7%) say they do something else. Of note, college-educated women show a higher tendency to keep their finances separate from their partners (64% merge, 21% separate, 15% something else).

- Middle-income Americans are saving less for retirement. The percentage of people putting less money into their retirement accounts has increased 7 points over the past two years even as 60% do not believe they are saving enough to retire comfortably.

- Rising cost of necessities remains an issue. Most middle-income Americans (88%) say recent increases in food prices have impacted them and their family. Individuals report having to buy cheaper options for similar products (68%), buy less food (54%), change their eating habits (48%), use coupons more frequently (37%), and buy more in bulk (30%).

Primerica Financial Security Monitor™ (FSM™) Topline Trends Data

|

|

Mar. 2024 |

Dec. 2023 |

Sept. 2023 |

Jun. 2023 |

Mar.

|

Dec. 2022 |

Sep. 2022 |

Jun.

|

Mar. 2022 |

|

How would you rate the condition of your personal finances? (Reporting “Excellent” and “Good” responses.)

Analysis: Respondents remain split on their assessment of their personal finances. |

50% |

50% |

49% |

50% |

52% |

53% |

53% |

54% |

60% |

|

Overall, would you say your income is…? (Reporting “Falling behind the cost of living” responses.)

Analysis: Concern about meeting the increased cost of living dropped over the past year. |

67% |

68% |

72% |

71% |

72% |

72% |

75% |

75% |

67% |

|

Do you have an emergency fund that would cover an expense of $1,000 or more (for example, if your car broke down or you had a large medical bill)? (Reporting “Yes” responses.)

Analysis: The percentage of Americans who have an emergency fund that would cover an expense of $1,000 or more has remained steady over the past year. |

62% |

60% |

62% |

61% |

58% |

59% |

60% |

61% |

62% |

|

How would you rate the economic health of your community? (Reporting “Not so good” and “Poor” responses.)

Analysis: Respondents’ rating of the economic health of their communities has gotten worse over the past year. |

60% |

57% |

55% |

54% |

59% |

53% |

55% |

58% |

52% |

|

How would you rate your ability to save for the future? (Reporting “Not so good” and “Poor” responses.)

Analysis: A significant majority continue to feel it is difficult to save for the future. |

67% |

73% |

71% |

71% |

73% |

74% |

73% |

72% |

66% |

|

In the past three months, has your credit card debt…? (Reporting “Increased” responses.)

Analysis: Credit card debt has remained steady over the past year. |

34% |

35% |

34% |

33% |

33% |

39% |

37% |

29% |

25% |

About Primerica’s Middle-Income Financial Security Monitor™ (FSM™)

Since September 2020, the Primerica Financial Security Monitor™ has surveyed middle-income households quarterly to gain a clear picture of their financial situation, and it coincides with the release of the monthly HBI™ four times annually. Polling was conducted online from March 6-11, 2024. Using Dynamic Online Sampling, Change Research polled 1,312 adults nationwide with incomes between $30,000 and $130,000. Post-stratification weights were made on gender, age, race, education and Census region to reflect the population of these adults based on the five-year averages in the 2021 American Community Survey, published by the U.S. Census. The margin of error is 3.0%. For more information visit Primerica.com/public/financial-security-monitor.html.

About the Primerica Household Budget Index™ (HBI™)

The Primerica Household Budget Index™ (HBI™) is constructed monthly on behalf of Primerica by its chief economic consultant Amy Crews Cutts, PhD, CBE®. The index measures the purchasing power of middle-income families with household incomes from $30,000 to $130,000 and is developed using data from the U.S. Bureau of Labor Statistics, the US Bureau of the Census, and the Federal Reserve Bank of Kansas City. The index looks at the cost of necessities including food, gas, utilities, and health care and earned income to track differences in inflation and wage growth.

The HBI™ is presented as a percentage. If the index is above 100%, the purchasing power of middle-income families is stronger than in the baseline period and they may have extra money left over at the end of the month that can be applied to things like entertainment, extra savings, or debt reduction. If it is under 100%, households may have to reduce overall spending to levels below budget, reduce their savings or increase debt to cover expenses. The HBI™ uses January 2019 as its baseline. This point in time reflects a recent “normal” economic time prior to the COVID-19 pandemic.

Periodically, prior HBI™ values may be revised due to revisions in the CPI series and Consumer Expenditure Survey releases by the U.S. Bureau of Labor Statistics (BLS). Beginning with the October 2023 release of the HBI™ data, health insurance costs will no longer be included in the calculation of the HBI™ data as part of the healthcare component because of some newly acknowledged methodology that has been used by the BLS to calculate the health insurance CPI. The health insurance CPI, as calculated by BLS, does not measure consumer costs of health insurance such as the cost of premiums paid or a combination of premiums and deductibles, but rather premium values retained by health insurers we do not believe it accurately reflects consumer experiences. The healthcare component will continue to include medical services, prescription drugs and equipment. Prior published values have been adjusted to reflect this change. For more information visit householdbudgetindex.com.

About Primerica, Inc.

Primerica, Inc., headquartered in Duluth, GA, is a leading provider of financial products and services to middle-income households in North America. Independent licensed representatives educate Primerica clients about how to better prepare for a more secure financial future by assessing their needs and providing appropriate solutions through term life insurance, which we underwrite, and mutual funds, annuities and other financial products, which we distribute primarily on behalf of third parties. We insured over 5.7 million lives and had over 2.9 million client investment accounts on December 31, 2023. Primerica, through its insurance company subsidiaries, was the #3 issuer of Term Life insurance coverage in the United States and Canada in 2022. Primerica stock is included in the S&P MidCap 400 and the Russell 1000 stock indices and is traded on The New York Stock Exchange under the symbol “PRI”.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240408765232/en/

Public Relations

Gana Ahn, 678-431-9266

gana.ahn@primerica.com

Investor Relations

Nicole Russell, 470-564-6663

nicole.russell@primerica.com

Source: Primerica, Inc.

Released April 9, 2024